Artificial intelligence (AI) titan Nvidia is priced for perfection in an imperfect market.

For nearly three years, the rise of artificial intelligence (AI) has dominated discussion on Wall Street. The prospect of AI-empowered software and systems making split-second decisions without the oversight of humans is a game-changer that the analysts at PwC believe can add $15.7 trillion to the global economy by the turn of the decade.

No company has been a more direct beneficiary of the evolution of AI than Nvidia (NVDA 1.75%). Since 2023 began, Nvidia has gone from being a tech company of fringe importance to the most-valuable publicly traded company at north of $4 trillion.

Image source: Nvidia.

Nvidia’s ascension is a reflection of its AI-graphic processing units (GPUs) being the bee’s knees among businesses operating high-compute data centers. Orders for Nvidia’s Hopper (H100) and Blackwell GPUs are backlogged, which has allowed the company to charge a triple-digit percentage premium for its hardware, when compared to other external competitors.

CEO Jensen Huang is doing his part to ensure that his company remains the compute leader in the AI space. Huang anticipates bringing a new advanced AI chip to market annually, with Blackwell Ultra (2025), Vera Rubin (2026), and Vera Rubin Ultra (2027) next in line. The latter two will operate on the all-new Vera processor.

Lastly, Nvidia’s CUDA software platform has tied everything together. CUDA is what developers use to maximize the compute potential of their Nvidia hardware. It’s effectively the hook that keeps buyers loyal to Nvidia’s ecosystem.

For Wall Street and investors, arguably nothing is of greater importance than Nvidia’s fiscal second-quarter operating results on Aug. 27 (Nvidia’s fiscal year ends in late January). While most analysts are counting on another blowout performance, there are no fewer than five reasons the party can end on Aug. 27 for the face of the AI revolution.

1. Internal competition begins pressuring margins

For most investors, external competition is viewed as the greatest threat to Nvidia’s AI-GPU dominance. Direct rivals include the likes of Advanced Micro Devices and China-based Huawei, among others.

Though the number of GPUs becoming available from external competitors is climbing with each passing quarter, this isn’t the threat investors should be worried about. The biggest risk to Nvidia comes from within.

Many of Nvidia’s largest customers by net sales (think members of the “Magnificent Seven”) are developing AI-GPUs to deploy in their data centers. While these chips aren’t going to compete with Nvidia’s hardware on the open market, they’re dangerous to Nvidia’s growth for a number of reasons:

- They’re reducing AI-GPU scarcity, which Nvidia has used to pump up its pricing power and boost its gross margin.

- They’re notably cheaper than Nvidia’s hardware, which can provide additional downside pressure on Nvidia’s pricing power.

- Unlike Nvidia’s GPUs, they aren’t going to be backlogged. This can slow upgrade cycles, which would weaken Nvidia’s future growth forecasts.

2. President Trump’s reciprocal tariffs introduce forecast uncertainty

A second headwind that can trip up the face of the AI revolution is President Donald Trump’s tariff and trade policy.

On April 2, the president unveiled a 10% global tariff, along with higher “reciprocal tariffs” on dozens of countries deemed to have adverse trade imbalances with America. These reciprocal tariff rates were paused for 90 days on April 9, and extended once more on July 7 via executive order to August 1. One week from today, they go into effect.

What’s so worrisome about Trump’s tariff and trade policy is that it introduces uncertainty into a situation (for Nvidia) where perfection and transparency have been priced in. If trade deals aren’t reached, retaliatory tariffs, supply chain hiccups, and higher prices that adversely impact margins, can all come into play.

The point being that Nvidia’s growth forecast is anything but certain, as of this writing on July 22.

Jensen Huang delivering his keynote address at GTC. Image source: Nvidia.

3. Jensen Huang’s innovation cycle begins to ruffle feathers

Something else that can ruffle Wall Street’s feathers and knock Nvidia off of its pedestal is the company’s innovation cycle.

Typically, aggressive spending to develop new technology is rewarded handsomely by investors. But there’s a fine line between technological advancements and maintaining a 70%-plus gross margin by charging a triple-digit premium to external competitors.

For example, Huang’s goal of bringing a new AI-GPU to market annually runs the risk of rapidly depreciating the value of prior-generation chips. If the value of Hopper GPUs tanks, customers that made the largest purchases of Hopper GPUs, along with data centers leasing out compute capacity, are going to be less likely to upgrade to new chips.

The other possibility is that as Nvidia introduces faster and higher-priced GPUs, businesses will simply opt for prior-generation chips at a discounted price. We may begin to see this reflected in the form of a weaker gross margin forecast from the company.

4. The Trump administration flip-flops on export restrictions

Since October 2022, the Joe Biden and Donald Trump administrations have restricted exports of high-powered AI chips and related equipment to China. Even though Nvidia had specifically developed toned-down versions of its highest-powered AI chips, both administrations had nixed its ability to export to the world’s No. 2 economy.

The silver lining is that the Trump administration recently (less than two weeks ago) reversed its export ban, which allows Nvidia to sell its less-advanced H20 chip to China. While this news sent Nvidia’s stock soaring, it makes the dangerous assumption that the Trump administration won’t flip-flop on this decision.

Though U.S. Commerce Secretary Howard Lutnick has suggested that allowing AI chip sales to China will keep companies reliant on American technology, President Trump and his administration have altered tariff and trade policy more times than can be counted over the last six months. No trade deal has been reached with China, and there remains the possibility that Nvidia’s technology is used as a bargaining chip for Trump to get what he wants.

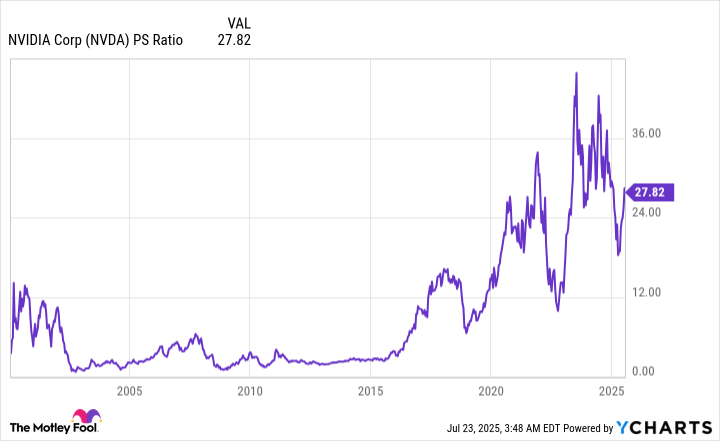

NVDA PS Ratio data by YCharts. PS Ratio= price-to-sales ratio.

5. History finally catches up with Nvidia’s premium valuation

The fifth and final reason the party can end for Nvidia on Aug. 27 is if history finally catches up to its outsized valuation.

I’m a firm believer that companies with sustainable moats and monopoly like market share deserve a premium valuation… to a point. Last summer, Nvidia stock tipped the scales at a price-to-sales (P/S) ratio of 42, which is more or less in-line with the peak trailing-12-month (TTM) P/S ratios of Wall Street’s leading businesses prior to the dot-com bubble bursting.

Despite Nvidia’s sales skyrocketing over the last two years, its P/S ratio on a TTM basis is still 28, as of July 22. No market-leading company has ever been able to sustain such a high premium over an extended period. What this suggests is that Nvidia has zero margin for error and its stock will be punished for the slightest miss or perceived uncertainty.